IR35: July update

A political hot potato that’s causing alarm, confusion and concern. No, not Brexit. Another one.

IR35.

Or, in the words of Her Majesty’s Revenue and Customs, “intermediaries legislation”. Or “off-payroll working”.

Put to one side for a moment – if that’s at all possible – Brexit, the possible prorogation of Parliament, and all talk of Johnson, Hunt, remain and leave, and consider other political moves that will have far-reaching consequences for huge numbers of people and across numerous industries.

A quick recap: what is IR35?

IR35 is:

- Tax legislation that in the government’s language is “designed to ensure fairness between individuals working in a similar way”. In everyone else’s language, it might be argued, IR35 is designed to generated revenue for HMRC by tackling tax avoidance by people who supply their services to clients via an intermediary, such as a limited company, but who would be an employee if the intermediary was not used.

- Being extended to the private sector in April 2020 having been introduced to the public sector in 2000.

- Seen as unfair by many because some contractors are having to pay employment taxes without benefiting from employment rights. Deemed to be ‘inside IR35’, those contractors are taxed in the same way as employees even though they may not be eligible for holiday pay, sick pay or other benefits.

- Both important and evolving – this is Frame 25’s fifth update on the subject.

- Explained in plain-English detail in these Frame 25 blog posts:

- Named after the Budget press release which first proposed the legislation in 1999 (it was introduced a year later, after extensive consultation).

Why’s IR35 in the news again?

Because on 11 July, HMRC published draft legislation for the next Finance Bill which ensures that from April next year…

- “Large digital businesses pay a new Digital Services Tax that reflects the value derived from their UK users”

- “Off-payroll working rules will ensure that two people working side by side in a similar role for the same employer pay the same employment taxes”

The rules will therefore mirror those introduced to the public sector in April 2017.

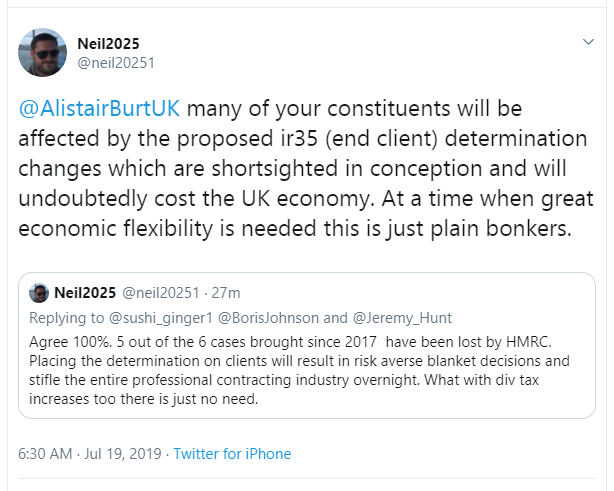

HMRC hasn’t listened to industry’s concerns and is simply continuing with its plans, as widely expected:

And this bit’s key:

To clarify and confirm the most important line in that excerpt: the onus is now on the hiring company, the business that has brought in the contractor, rather than the freelancer herself or himself.

The measure is expected to bring in £3.1 billion in additional revenues for HMRC between 2020 and 2024, although a number of groups have said a list of their concerns has been largely ignored by the government.

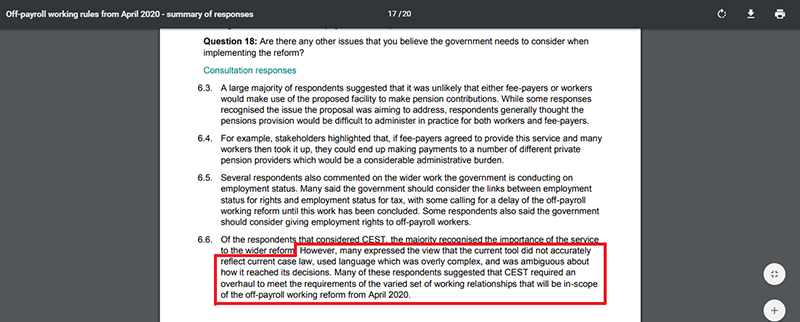

People have suggested HMRC delay the reform, establish an independent appeal process and improve the Check Employment Status for Tax (CEST) tool, its online status checker.

Here’s a summary of responses, a key one being:

So what can we do, as an industry?

What can you do as a hiring company?

And options do individuals have?

As alluded to above, the end client in the supply chain will hold the responsibility for any liabilities until they pass on a ‘status determination statement’ to the party they contract with (ie the limited company, the personal service company or the agency) and the worker.

The determination statement must include the reasons why the decision was reached, ensuring that reasonable care had been taken when arriving at the decision.

Contractors can dispute the determination, which must be done directly with the client.

End clients will have 45 days to respond if they disagree with a challenge, and must provide the worker with the reasons why they believe their determination was correct.

What are we doing to prepare?

Our Clients

We are discussing IR35 determinations with clients across the industry.

Businesses will need to ensure that they have robust procedures in place to meet their ongoing obligations and be ready for implementation.

This is key preparation time, to be spent auditing the contract workforce and the roles they perform.

Retaining Talent

Once determinations have been made it’s likely that clients will face the following issues:

- Existing limited company contractors shall now face an increased level of tax when engaged through a PAYE scheme.

- Medium and large companies must decide whether to increase rates to mitigate the loss contractors face, whilst also increasing costs for engaging contractors with 13.8% employer’s NI contribution.

- Simply outsourcing payroll to a third party using an umbrella company is likely to then charge a fee on to the contractor for using their services, and therefore will likely increase the risk of being able to retain talent.

Our Contractors

We are advising contractors of their options, educating professionals on the topic and explaining key factors behind IR35 determination – supervision, direction and control.

We have a number of services we offer PAYE contractors to ensure migrating to a payroll is simple and straightforward.

Netflix, Paramount and Warner Bros.: What the Deal Means for the Broadcast and Production Industry

How the Employment Rights Act 2025 Is Reshaping the Freelance Market